Boston Area Multi-Family Market Report for Q3 2026

Overview

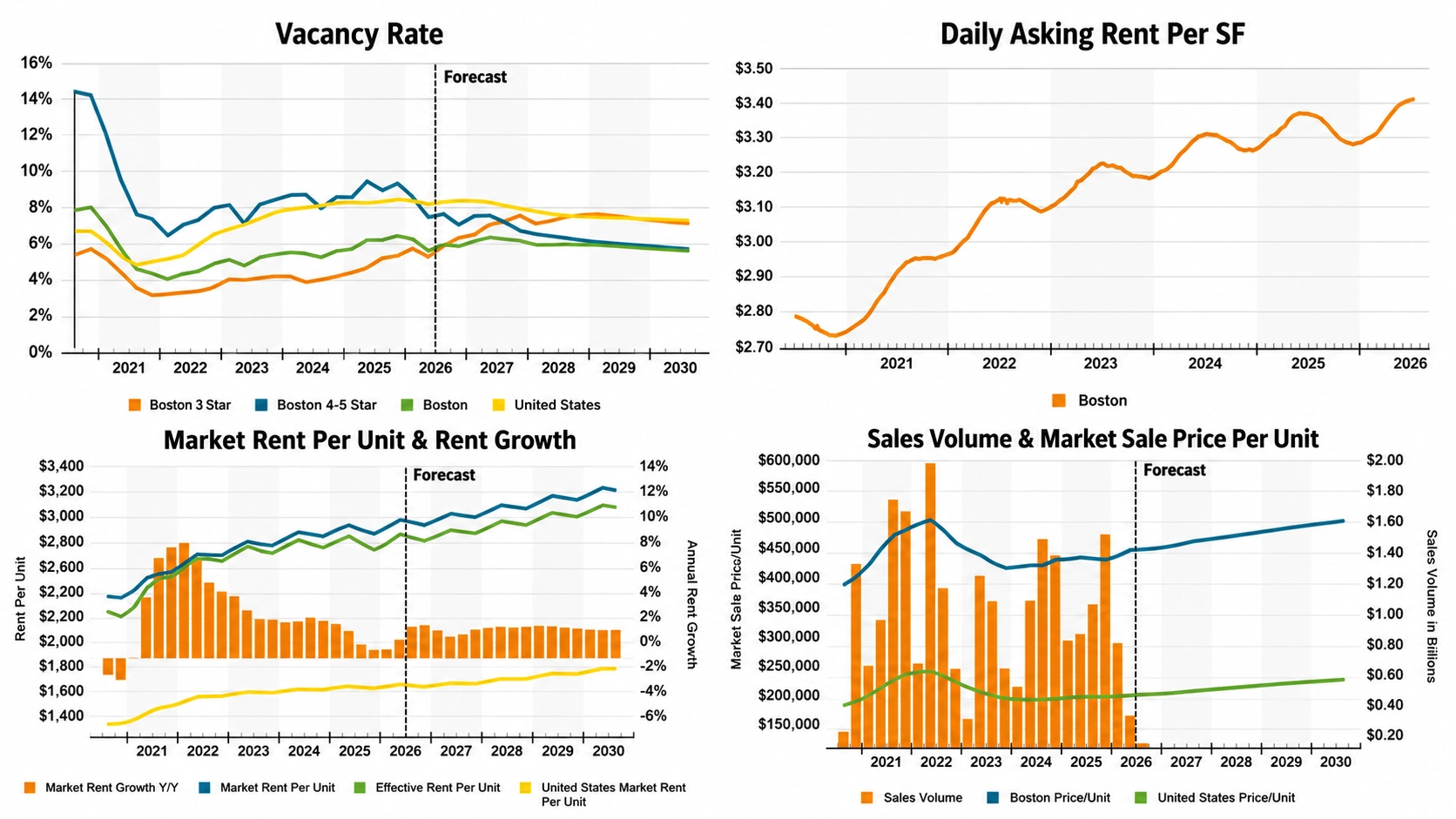

Boston’s multifamily market continues to show healthy fundamentals despite a modest rise in vacancy driven by new supply. As of the third quarter of 2026, the vacancy rate stands at 5.7%, slightly below the three-year average of 5.8%. Strong leasing activity helped absorb more than 8,500 units over the past year, although demand was still countered by approximately 7,100 newly delivered units.

Market demand has strengthened considerably, with leasing activity up roughly 59% compared to the same period last year. By the end of the first quarter, tenant demand exceeded new deliveries for the first time since the third quarter of 2024, signaling improving market balance. At the same time, construction activity continues to slow, with units under construction declining each quarter since late 2024.

The development pipeline is expected to continue shrinking through 2026. After averaging nearly 8,500 new units annually between 2023 and 2025, deliveries are forecast to decline by about 30% year over year. Even with this slowdown, Boston remains one of the most active multifamily development markets in the Northeast, outperforming peers such as Philadelphia and Northern New Jersey.

Rent growth has moderated as new supply entered the market, with asking rents increasing 1.4% year over year as of the third quarter. While this is down significantly from the near double-digit gains recorded in early 2022, rent growth is expected to accelerate toward year-end and remain above the national average. Boston’s vacancy rate also remains well below national levels, with the gap now approximately 200 basis points.

Investment activity has remained steady, with multifamily properties accounting for roughly 32% of Boston’s total investment volume in the first quarter. Looking ahead, vacancy is expected to rise modestly before peaking near 6.7% by mid-year, while rent growth approaches 2% by year-end. Although economic uncertainty could weigh on performance, Boston’s strong leasing momentum and status as a premier gateway market should continue to support long-term demand.