Boston’s office market has shown encouraging signs of recovery in 2026, driven by strong leasing demand and renewed activity in the life sciences sector. Leasing volume has remained steady year over year, with several large expansions and relocations contributing to positive momentum. Demand remains concentrated in trophy and Class A properties, where available space continues to decline.

Office attendance has also improved. According to Placer.ai, Boston office attendance rose 11.2% year over year in early spring 2026, one of the strongest gains among major U.S. markets. While the city has recovered to about 66% of pre-pandemic attendance levels—still below the national average of 73.5%—the trend remains positive as more companies strengthen return-to-office policies, including Fidelity Investments’ planned five-day in-office schedule beginning in September.

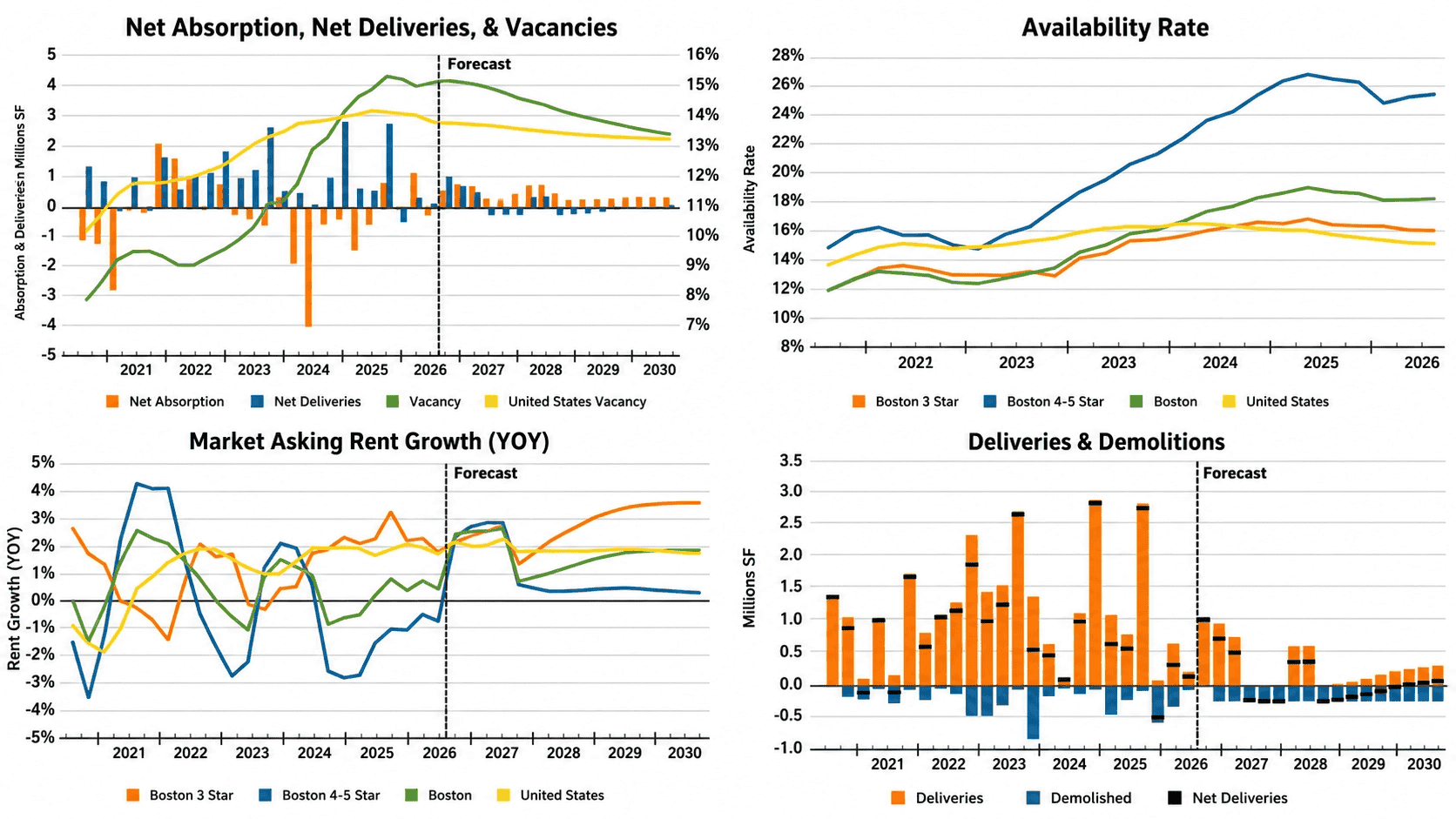

Improving attendance has translated into stronger market performance. Tenants absorbed roughly 730,000 square feet over the past 12 months, and Boston recorded approximately 1.1 million square feet of positive net absorption in the first quarter—the first quarterly gain since 2022. Much of this activity has been driven by relocations and consolidations into higher-quality 4- and 5-star office buildings, while tenant move-outs have declined compared to prior periods.

Despite these gains, vacancy remains elevated at 15.3%, exceeding the national average of 13.9%. Vacancy has risen nearly 200 basis points over the past three years due in part to new office and life science developments delivering significant amounts of uncommitted space. At the same time, the market continues to see older office properties converted to residential use, while much of the remaining development pipeline is geared toward life science and biotechnology users.

Rent growth has remained modest, increasing 1.7% annually, slightly below the national average of 2.0%. However, Boston’s asking rents remain above national levels, supported by relatively limited concessions and shorter free-rent periods. Looking ahead, continued leasing activity, improved office utilization, and a shrinking construction pipeline should support recovery, although vacancy is expected to remain near historic highs and rent growth is likely to stay subdued in the near term.