By Mile Sobolik

Source: Invesco

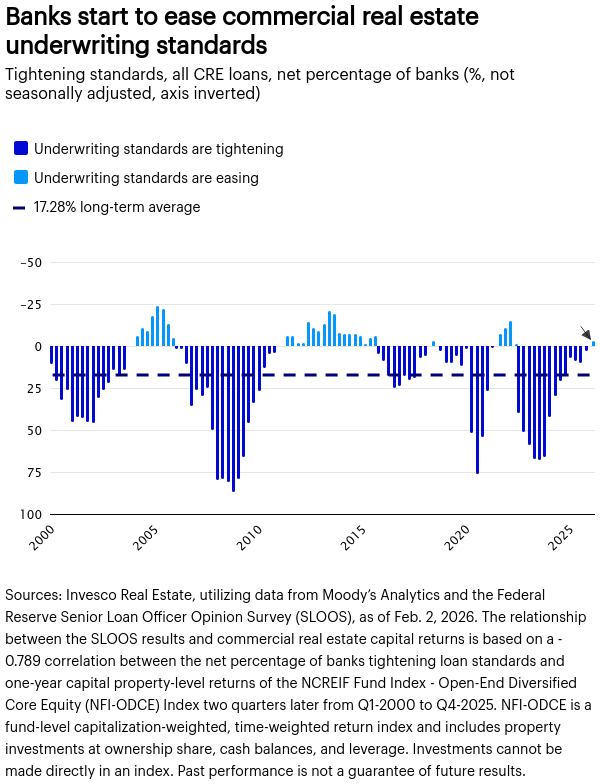

US commercial real estate (CRE) got an encouraging signal. Banks have begun to ease underwriting standards for CRE loans for the first time since interest rates started rising in 2022, according to the January 2026 Senior Loan Officer Opinion Survey (SLOOS) from the Federal Reserve. It suggests lenders are gaining confidence that market conditions have stabilized and that risks are becoming more manageable.

This shift toward easing is expected to boost CRE loan origination activity and support property transaction growth, broadening investment opportunities within CRE equity and credit. Similar turns in lending standards have historically tended to occur early in recovery phases, often marking the start of a new capital cycle. Comparable patterns followed the tech downturn in the early 2000s, the post–Global Financial Crisis period beginning in 2011, and the economic reopening after the COVID-19 era stimulus in 2021–2022. (See the chart below.)

The January 2026 SLOOS reported a net tightening of -3.16% (negative numbers reflect net easing) across combined CRE loan types, including construction and land development loans, loans secured by nonfarm, nonresidential properties (e.g., office, retail, industrial), and multi-family loans. Anything less than zero means underwriting standards are easing; greater than zero means underwriting standards are tightening.

Banks start to ease commercial real estate underwriting standards

Combination chart with 3 data series.

Tightening standards, all CRE loans, net percentage of banks (%, not seasonally adjusted, axis inverted)

Sources: Invesco Real Estate, utilizing data from Moody’s Analytics and the Federal Reserve Senior Loan Officer Opinion Survey (SLOOS), as of Feb. 2, 2026. The relationship between the SLOOS results and commercial real estate capital returns is based on a -0.789 correlation between the net percentage of banks tightening loan standards and one-year capital property-level returns of the NCREIF Fund Index – Open-End Diversified Core Equity (NFI-ODCE) Index two quarters later from Q1-2000 to Q4-2025. NFI-ODCE is a fund-level capitalization-weighted, time-weighted return index and includes property investments at ownership share, cash balances, and leverage. Investments cannot be made directly in an index. Past performance is not a guarantee of future results. Banks start to ease commercial real estate underwriting standards are tightening.

While modest, if this shift into net easing continues into future quarters, it could support a gradual improvement in commercial property values and movement into a virtuous cycle of more CRE transactions and opportunity. While loan originations are expected to grow broadly across lender types, market share over recent years has moved up significantly for private non-bank CRE lenders, which averaged 4.6% of total CRE loan originations from 2010–2020. Post-pandemic, their share averaged 8.6% from 2021 through Q3-2025.1

Footnotes

- 1 Source: Invesco Real Estate, utilizing data from Mortgage Bankers Association as of Nov. 6, 2025, most recent data available. Loan origination market share for private non-bank CRE lenders averaged 4.6% of total CRE loan originations from 2010–2020. Post-pandemic, their share has averaged 8.6% from 2021 through Q3 -2025.