By Jordan Erb

Source: Bloomberg

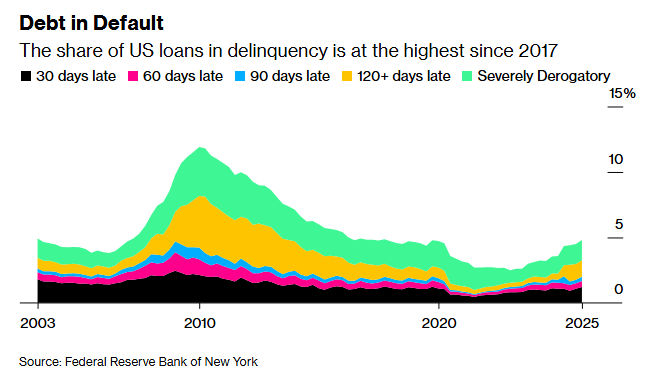

Delinquency rates on loans ranging from mortgages to credit cards rose to 4.8% of all outstanding US household debt in the fourth quarter, the highest level since 2017, driven by rising defaults among low-income and young borrowers.

While the overall share of loans in some stage of default is near pre-pandemic averages, the rise in delinquencies among the lowest earners adds to evidence of an increasingly bifurcated economy, data from the Federal Reserve Bank of New York’s Quarterly Report on Household Debt and Credit released Tuesday showed.

The rise in defaults was driven by delinquencies in mortgage payments, with New York Fed researchers finding them particularly high in lower-income zip codes. Student-loan delinquencies, which have surged following the end of a pandemic pause in payment requirements and Donald Trump’s new effort to crack down on indebted student borrowers, have contributed to the rise in defaults.

The rise in defaults was driven by delinquencies in mortgage payments, with New York Fed researchers finding them particularly high in lower-income zip codes. Student-loan delinquencies, which have surged following the end of a pandemic pause in payment requirements and Donald Trump’s new effort to crack down on indebted student borrowers, have contributed to the rise in defaults.

The increased struggle among low-income and young borrowers unable to pay their loans is consistent with elevated unemployment rates among some parts of the US population. The jobless rate for workers 16 to 24 years old stood at 10.4% in December, near the highest levels since the depths of the pandemic.