The Quick Answer: When Will Multifamily Vacancy Peak?

Multifamily vacancy in the United States is expected to continue rising through 2026 and potentially peak around early 2027, driven primarily by a historic surge in new apartment supply and slower demand growth.⁴ However, the exact timing is uncertain and depends heavily on how quickly new units are absorbed, how supply pipelines evolve, and how vacancy is measured across markets.

Why Multifamily Vacancy Is Rising in 2025–2026

The U.S. multifamily sector is currently working through one of the largest supply waves in decades. Over the past several years, developers have delivered a substantial number of new units, creating a mismatch between supply and demand. According to MMCG’s 2026 outlook, this imbalance pushed national vacancy to approximately 8.6 percent, well above long-term averages.¹

At the same time, demand has moderated. While renter demand remains positive, it has slowed relative to the pace of new deliveries, reducing the ability of the market to absorb new units quickly.¹ The National Association of Home Builders (NAHB) similarly reports that vacancy continues to increase as supply enters the market and demand softens amid a weaker labor environment.²

Even as construction starts decline, the backlog of projects already underway ensures that new inventory will continue entering the market in the near term. Yardi Matrix forecasts more than one million units will be delivered between 2026 and 2028, extending supply pressure well beyond the initial construction peak.⁵

Regional Differences: Where Vacancy Is Highest

Vacancy trends are not uniform across the United States. Instead, rising vacancy is concentrated in specific regions where supply growth has been most intense. CBRE research shows that regions such as the South Central, Mountain, and Southwest have experienced the greatest pressure due to large numbers of newly delivered units still in the lease-up phase.³

By contrast, markets with less development activity—particularly in parts of the Midwest and Northeast—have shown more stable rent growth and occupancy conditions.³ This divergence suggests that the expected “peak” in vacancy will not occur uniformly across the country but will instead reflect a combination of localized cycles.

Hidden Vacancy: The Role of Lease-Up and Measurement

An important factor affecting vacancy forecasts is how vacancy is measured. Standard industry metrics often exclude newly delivered buildings that have not yet reached stabilized occupancy levels.³

When these “pre-stabilized” properties are included, CBRE estimates that vacancy rates are significantly higher than reported figures during periods of heavy construction.³ This means that the true extent of vacancy may be understated in headline statistics, and that the peak in vacancy could occur later or at a higher level than commonly perceived.

The lease-up process introduces an additional lag. Even after construction is completed, properties require time to fill units, which delays the stabilization of occupancy levels and prolongs elevated vacancy conditions.

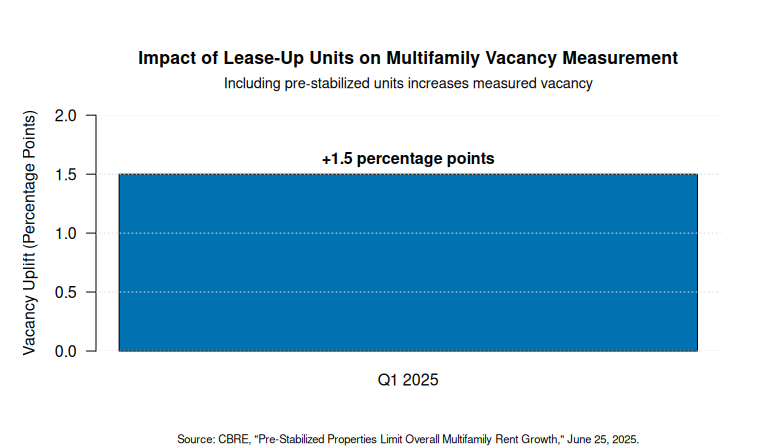

Figure 1. Impact of Lease‑Up Units on Multifamily Vacancy Measurement (Q1 2025).

Including newly delivered (“pre‑stabilized”) apartment units increases measured U.S. multifamily vacancy rates by approximately 1.5 percentage points, highlighting how standard vacancy metrics may understate true market conditions.

When Will Multifamily Vacancy Peak?

Industry forecasts broadly agree that vacancy will remain elevated before eventually stabilizing. CoStar analysis explicitly projects that vacancy will rise further and peak in early 2027, reflecting the lag between supply delivery and full absorption.⁴

Other research supports the timing indirectly. Yardi Matrix data shows that supply deliveries will continue through at least 2027, indicating that inventory pressures will persist even as new construction slows.⁵ Meanwhile, Cushman & Wakefield reports that vacancy has already stabilized in recent periods, suggesting that the market is transitioning toward equilibrium.⁷

Data from Arbor Realty Trust, based on Moody’s Analytics, indicates that vacancy may already be entering a plateau phase as absorption begins to align more closely with new supply.⁶

Taken together, these sources suggest that vacancy is unlikely to peak at a single precise moment. Instead, it is more likely to plateau across 2026–2027, with conditions varying by market and asset class.

What Could Change the Vacancy Outlook

Although the general trajectory of rising vacancy followed by stabilization is widely supported, several factors could shift the timing or magnitude of the peak.

First, demand trends will play a critical role. If household formation strengthens or renter demand accelerates, absorption could increase, leading to an earlier stabilization of vacancy. Conversely, continued economic softness could delay absorption and prolong elevated vacancy levels.²

Second, supply dynamics remain crucial. While construction starts have declined, ongoing project completions will continue adding inventory in the near term.⁵ Delays in construction timelines or extended delivery schedules could push vacancy pressures further into the future.

Third, lease-up timing will affect the observed peak. Newly delivered units that remain unoccupied during lease-up phases contribute to vacancy longer than stabilized inventory, extending the period of elevated vacancy.³

Finally, differences in measurement—particularly whether pre-stabilized units are included—can significantly influence how vacancy trends are interpreted, making the peak appear earlier or later depending on the methodology used.³

Key Takeaways for the 2026–2027 Multifamily Outlook

The multifamily market is moving through a period of adjustment following a historic supply surge. Vacancy rates are elevated, demand remains positive but tempered, and regional divergence is reshaping national trends.

While forecasts such as CoStar’s point to a peak in early 2027, the broader body of research indicates that this should be understood as a range rather than a fixed point in time. The interplay between supply delivery, demand absorption, and lease-up dynamics suggests that vacancy may plateau across multiple quarters rather than decline abruptly.

Ultimately, the timing and severity of the vacancy peak will vary across markets, with oversupplied regions experiencing more pronounced and prolonged pressure than supply-constrained areas. As a result, market-level analysis remains critical for understanding where and when conditions will normalize.

Footnotes

- MMCG Invest, “U.S. Multifamily Market Outlook 2026: Current Conditions, Investment Trends, and Five-Year Forecast,” March 2026. [moodyscre.com]

- National Association of Home Builders (NAHB), “Multifamily Market Expected to Cool in 2026 as Vacancies Rise,” February 17, 2026. [costar.com]

- CBRE, “Pre-Stabilized Properties Limit Overall Multifamily Rent Growth,” June 25, 2025.

- CoStar, “Rising Multifamily Vacancy Expected to Peak in Early 2027,” May 5, 2026. [cushmanwakefield.com]

- Yardi Matrix, “U.S. Multifamily Rent, Supply and Completions Data,” February 10, 2026. [cbre.com]

- Arbor Realty Trust, “U.S. Multifamily Market Snapshot — August 2025,” August 12, 2025. [pwc.com]

- Cushman & Wakefield, “U.S. Multifamily MarketBeat Q1 2026,” 2026. [mmcginvest.com]